Phân Tích Rủi Ro và Lợi Nhuận Danh Mục Đầu Tư (Portfolio)

Giới Thiệu

Phân tích rủi ro và lợi nhuận danh mục đầu tư là một phần quan trọng trong quản lý đầu tư. Bài viết này sẽ giúp bạn hiểu rõ về các khái niệm cơ bản và cách phân tích hiệu quả danh mục đầu tư của mình.

Các Chỉ Số Quan Trọng

1. Tỷ Suất Sinh Lợi (Return Rate)

Tỷ suất sinh lợi là thước đo hiệu quả của khoản đầu tư:

def calculate_return_rate(initial_value, final_value):

return ((final_value - initial_value) / initial_value) * 100

2. Rủi Ro (Risk)

Rủi ro được đo lường bằng độ lệch chuẩn của lợi nhuận:

import numpy as np

def calculate_risk(returns):

return np.std(returns) * np.sqrt(252) # Annualized volatility

3. Tỷ Lệ Sharpe (Sharpe Ratio)

Đo lường lợi nhuận điều chỉnh theo rủi ro:

def calculate_sharpe_ratio(returns, risk_free_rate):

excess_returns = returns - risk_free_rate

return np.mean(excess_returns) / np.std(excess_returns) * np.sqrt(252)

Phân Tích Danh Mục

1. Đa Dạng Hóa (Diversification)

Đa dạng hóa giúp giảm rủi ro tổng thể:

- Phân bổ tài sản

- Tương quan giữa các tài sản

- Tái cân bằng định kỳ

2. Tối Ưu Hóa Danh Mục

Sử dụng Modern Portfolio Theory (MPT):

def optimize_portfolio(returns, cov_matrix):

num_assets = len(returns)

weights = np.random.random(num_assets)

weights = weights / np.sum(weights)

return weights

3. Phân Tích Kịch Bản

Đánh giá hiệu suất trong các điều kiện thị trường khác nhau:

- Thị trường tăng

- Thị trường giảm

- Thị trường biến động

Công Cụ Phân Tích

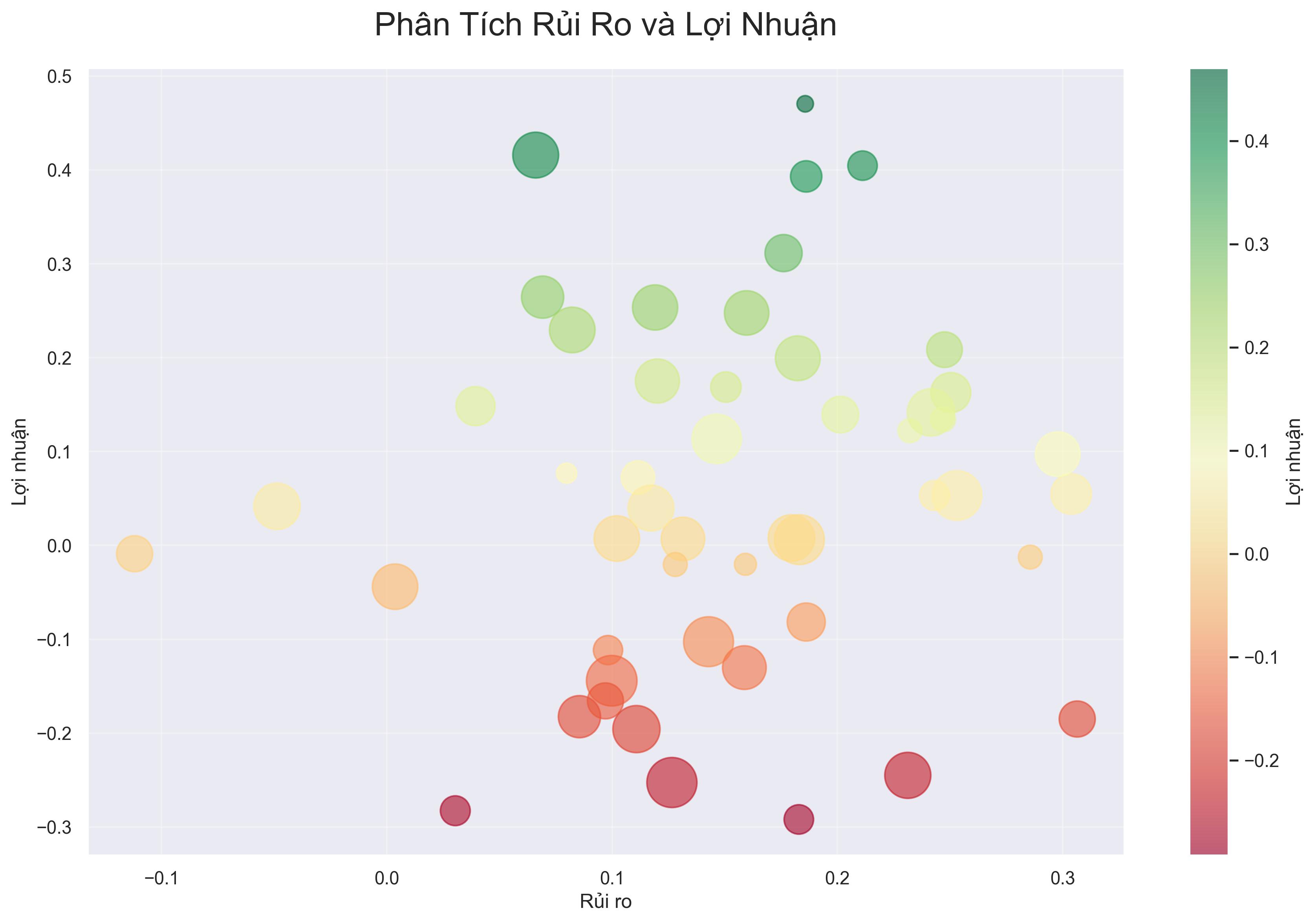

1. Biểu Đồ Phân Tán (Scatter Plot)

import matplotlib.pyplot as plt

def plot_risk_return(risks, returns, labels):

plt.scatter(risks, returns)

for i, label in enumerate(labels):

plt.annotate(label, (risks[i], returns[i]))

plt.xlabel('Risk (Volatility)')

plt.ylabel('Expected Return')

plt.title('Risk-Return Profile')

plt.show()

2. Biểu Đồ Đường (Line Chart)

def plot_portfolio_value(portfolio_values, dates):

plt.plot(dates, portfolio_values)

plt.xlabel('Date')

plt.ylabel('Portfolio Value')

plt.title('Portfolio Performance Over Time')

plt.show()

Quản Lý Rủi Ro

1. Stop Loss

def calculate_stop_loss(entry_price, risk_percentage):

return entry_price * (1 - risk_percentage/100)

2. Position Sizing

def calculate_position_size(account_value, risk_per_trade, stop_loss_pips):

risk_amount = account_value * (risk_per_trade/100)

position_size = risk_amount / stop_loss_pips

return position_size

Báo Cáo Hiệu Suất

1. Thống Kê Cơ Bản

- Tỷ suất sinh lợi hàng năm

- Độ biến động

- Tỷ lệ Sharpe

- Drawdown tối đa

2. Phân Tích Nâng Cao

- Phân tích yếu tố

- Phân tích tương quan

- Phân tích rủi ro đuôi

Kết Luận

Phân tích rủi ro và lợi nhuận danh mục đầu tư là một quá trình liên tục. Bằng cách sử dụng các công cụ và phương pháp phù hợp, bạn có thể:

- Tối ưu hóa danh mục đầu tư

- Giảm thiểu rủi ro

- Tăng cường lợi nhuận

- Đưa ra quyết định đầu tư tốt hơn

Hãy luôn nhớ rằng quản lý rủi ro là yếu tố quan trọng nhất trong đầu tư. Một danh mục được quản lý tốt sẽ giúp bạn đạt được mục tiêu đầu tư dài hạn.