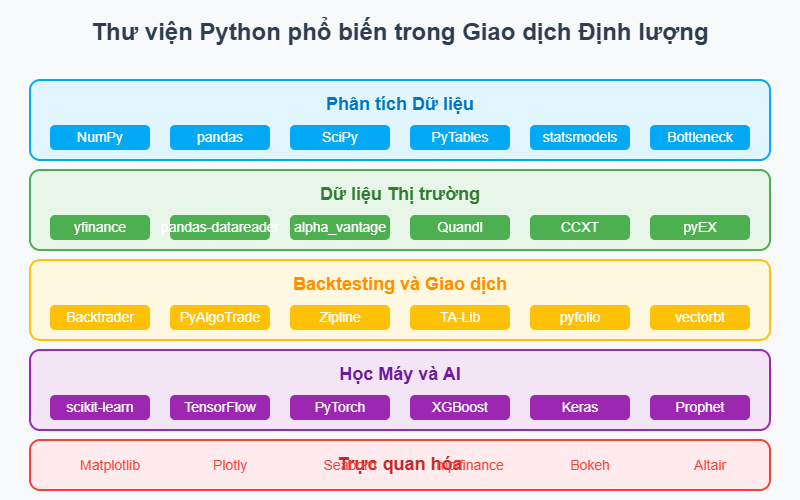

Các thư viện Python phổ biến nhất trong giao dịch định lượng

Giới thiệu

Giao dịch định lượng (Quantitative Trading) là lĩnh vực sử dụng các thuật toán, mô hình toán học và phân tích thống kê để tìm kiếm cơ hội và thực hiện các giao dịch trên thị trường tài chính. Python đã trở thành ngôn ngữ lập trình hàng đầu trong lĩnh vực này nhờ hệ sinh thái phong phú các thư viện chuyên dụng. Bài viết này trình bày tổng quan về các thư viện Python phổ biến nhất được sử dụng trong giao dịch định lượng, phân loại theo chức năng.

1. Thư viện phân tích dữ liệu

Các thư viện này là nền tảng cho việc phân tích dữ liệu tài chính, xử lý chuỗi thời gian và tính toán số học.

NumPy

NumPy là thư viện nền tảng cho tính toán khoa học với Python, cung cấp cấu trúc dữ liệu mảng đa chiều hiệu suất cao và các hàm toán học vector hóa.

import numpy as np

prices = np.array([100, 102, 104, 103, 105])

returns = np.diff(prices) / prices[:-1]

print(f"Lợi nhuận hàng ngày: {returns}")

print(f"Lợi nhuận trung bình: {np.mean(returns)}")

print(f"Độ lệch chuẩn: {np.std(returns)}")

pandas

pandas là thư viện phân tích dữ liệu cung cấp các cấu trúc dữ liệu linh hoạt như DataFrame, đặc biệt mạnh trong xử lý chuỗi thời gian tài chính.

import pandas as pd

df = pd.read_csv('stock_data.csv', parse_dates=['Date'], index_col='Date')

df['Returns'] = df['Close'].pct_change()

df['SMA_20'] = df['Close'].rolling(window=20).mean()

df['Volatility'] = df['Returns'].rolling(window=20).std() * np.sqrt(252)

print(df.head())

SciPy

SciPy xây dựng trên NumPy và cung cấp nhiều mô-đun cho các tác vụ khoa học và kỹ thuật, bao gồm tối ưu hóa, thống kê, và xử lý tín hiệu.

from scipy import stats

from scipy import optimize

returns = df['Returns'].dropna().values

k2, p = stats.normaltest(returns)

print(f"p-value cho kiểm định tính chuẩn: {p}")

def negative_sharpe(weights, returns, risk_free_rate=0.02):

portfolio_return = np.sum(returns.mean() * weights) * 252

portfolio_volatility = np.sqrt(np.dot(weights.T, np.dot(returns.cov() * 252, weights)))

sharpe = (portfolio_return - risk_free_rate) / portfolio_volatility

return -sharpe

stock_returns = pd.DataFrame()

constraints = ({'type': 'eq', 'fun': lambda x: np.sum(x) - 1})

bounds = tuple((0, 1) for _ in range(3))

result = optimize.minimize(negative_sharpe, np.array([1/3, 1/3, 1/3]),

args=(stock_returns,), bounds=bounds, constraints=constraints)

statsmodels

statsmodels cung cấp các lớp và hàm để ước lượng nhiều mô hình thống kê khác nhau, thực hiện kiểm định thống kê và khám phá dữ liệu thống kê.

import statsmodels.api as sm

from statsmodels.tsa.arima.model import ARIMA

X = df[['Feature1', 'Feature2', 'Feature3']]

X = sm.add_constant(X)

y = df['Returns']

model = sm.OLS(y, X).fit()

print(model.summary())

arima_model = ARIMA(df['Close'], order=(5, 1, 0))

arima_result = arima_model.fit()

forecast = arima_result.forecast(steps=30)

PyTables

PyTables là thư viện để quản lý lượng dữ liệu lớn, được thiết kế để xử lý hiệu quả các bảng dữ liệu rất lớn.

import tables

class StockData(tables.IsDescription):

date = tables.StringCol(10)

symbol = tables.StringCol(10)

open = tables.Float64Col()

high = tables.Float64Col()

low = tables.Float64Col()

close = tables.Float64Col()

volume = tables.Int64Col()

h5file = tables.open_file("market_data.h5", mode="w")

table = h5file.create_table("/", 'stocks', StockData)

row = table.row

for data in stock_data:

row['date'] = data['date']

row['symbol'] = data['symbol']

row['open'] = data['open']

row['high'] = data['high']

row['low'] = data['low']

row['close'] = data['close']

row['volume'] = data['volume']

row.append()

table.flush()

Bottleneck

Bottleneck là thư viện tối ưu hóa hiệu suất cho các hoạt động thường gặp trong NumPy/pandas.

import bottleneck as bn

rolling_mean = bn.move_mean(df['Close'].values, window=20)

rolling_max = bn.move_max(df['Close'].values, window=50)

rolling_median = bn.move_median(df['Close'].values, window=20)

max_idx = bn.argmax(df['Volume'].values)

max_volume_date = df.index[max_idx]

2. Thư viện thu thập dữ liệu thị trường

Các thư viện này giúp truy cập dữ liệu thị trường từ nhiều nguồn khác nhau.

yfinance

yfinance là thư viện phổ biến để tải dữ liệu tài chính từ Yahoo Finance, cung cấp dữ liệu lịch sử và thông tin công ty miễn phí.

import yfinance as yf

msft = yf.Ticker("MSFT")

hist = msft.history(period="1y")

print(hist.head())

data = yf.download(["AAPL", "MSFT", "GOOG"], start="2020-01-01", end="2023-01-01")

print(data['Close'].head())

info = msft.info

financials = msft.financials

pandas-datareader

pandas-datareader cung cấp giao diện truy cập dữ liệu từ nhiều nguồn như Fred, World Bank, Eurostat, và cả Yahoo Finance.

import pandas_datareader.data as web

from datetime import datetime

fed_data = web.DataReader('GDP', 'fred', start=datetime(2010, 1, 1), end=datetime.now())

print(fed_data.head())

wb_data = web.DataReader('NY.GDP.MKTP.CD', 'wb', start=2010, end=2020)

print(wb_data.head())

alpha_vantage

Thư viện Python cho API Alpha Vantage, cung cấp dữ liệu thị trường tài chính miễn phí và trả phí.

from alpha_vantage.timeseries import TimeSeries

from alpha_vantage.techindicators import TechIndicators

ts = TimeSeries(key='YOUR_API_KEY')

data, meta_data = ts.get_daily(symbol='AAPL', outputsize='full')

print(data.head())

ti = TechIndicators(key='YOUR_API_KEY')

rsi, meta_data = ti.get_rsi(symbol='AAPL', interval='daily', time_period=14, series_type='close')

print(rsi.head())

Quandl

Quandl cung cấp dữ liệu tài chính, kinh tế và thị trường thay thế từ nhiều nguồn (một số miễn phí, một số trả phí).

import quandl

quandl.ApiConfig.api_key = 'YOUR_API_KEY'

oil_data = quandl.get('EIA/PET_RWTC_D')

print(oil_data.head())

data = quandl.get("WIKI/AAPL", start_date="2010-01-01", end_date="2018-12-31")

print(data.head())

CCXT

CCXT (CryptoCurrency eXchange Trading Library) là thư viện cho 100+ sàn giao dịch tiền điện tử, hỗ trợ nhiều chức năng API.

import ccxt

binance = ccxt.binance({

'apiKey': 'YOUR_API_KEY',

'secret': 'YOUR_SECRET_KEY',

})

ticker = binance.fetch_ticker('BTC/USDT')

print(ticker)

ohlcv = binance.fetch_ohlcv('ETH/USDT', '1h')

df = pd.DataFrame(ohlcv, columns=['timestamp', 'open', 'high', 'low', 'close', 'volume'])

df['timestamp'] = pd.to_datetime(df['timestamp'], unit='ms')

print(df.head())

pyEX

Thư viện Python cho IEX Cloud API, cung cấp dữ liệu thị trường tài chính thời gian thực và lịch sử.

import pyEX as p

c = p.Client(api_token='YOUR_API_TOKEN')

df = c.chartDF('AAPL')

print(df.head())

company = c.company('TSLA')

print(company)

3. Thư viện backtesting và giao dịch

Các thư viện này giúp xây dựng, kiểm thử và triển khai chiến lược giao dịch.

Backtrader

Backtrader là framework phổ biến để thử nghiệm chiến lược giao dịch trên dữ liệu lịch sử, với thiết kế hướng đối tượng linh hoạt.

import backtrader as bt

class SMACrossStrategy(bt.Strategy):

params = (

('fast_length', 10),

('slow_length', 30),

)

def __init__(self):

self.fast_ma = bt.indicators.SMA(self.data.close, period=self.params.fast_length)

self.slow_ma = bt.indicators.SMA(self.data.close, period=self.params.slow_length)

self.crossover = bt.indicators.CrossOver(self.fast_ma, self.slow_ma)

def next(self):

if not self.position:

if self.crossover > 0:

self.buy()

elif self.crossover < 0:

self.sell()

cerebro = bt.Cerebro()

cerebro.addstrategy(SMACrossStrategy)

data = bt.feeds.PandasData(dataname=df)

cerebro.adddata(data)

cerebro.broker.setcash(100000)

cerebro.addsizer(bt.sizers.PercentSizer, percents=10)

print(f'Vốn ban đầu: {cerebro.broker.getvalue():.2f}')

cerebro.run()

print(f'Vốn cuối: {cerebro.broker.getvalue():.2f}')

cerebro.plot()

PyAlgoTrade

PyAlgoTrade là thư viện backtesting và giao dịch thuật toán, tập trung vào khả năng mở rộng và tích hợp dữ liệu trực tuyến.

from pyalgotrade import strategy

from pyalgotrade.barfeed import quandlfeed

from pyalgotrade.technical import ma

class MyStrategy(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, smaPeriod):

super(MyStrategy, self).__init__(feed, 100000)

self.__position = None

self.__instrument = instrument

self.__sma = ma.SMA(feed[instrument].getCloseDataSeries(), smaPeriod)

def onBars(self, bars):

bar = bars[self.__instrument]

if self.__sma[-1] is None:

return

if self.__position is None:

if bar.getClose() > self.__sma[-1]:

self.__position = self.enterLong(self.__instrument, 10)

elif bar.getClose() < self.__sma[-1] and not self.__position.exitActive():

self.__position.exitMarket()

feed = quandlfeed.Feed()

feed.addBarsFromCSV("orcl", "WIKI-ORCL-2000-quandl.csv")

myStrategy = MyStrategy(feed, "orcl", 15)

myStrategy.run()

print("Final portfolio value: $%.2f" % myStrategy.getBroker().getEquity())

Zipline

Zipline là thư viện backtesting được phát triển bởi Quantopian (đã đóng cửa), tập trung vào hiệu suất và khả năng mở rộng.

from zipline.api import order, record, symbol

from zipline.finance import commission, slippage

import matplotlib.pyplot as plt

def initialize(context):

context.asset = symbol('AAPL')

context.sma_fast = 10

context.sma_slow = 30

context.set_commission(commission.PerShare(cost=0.001, min_trade_cost=1.0))

context.set_slippage(slippage.FixedSlippage(spread=0.00))

def handle_data(context, data):

fast_sma = data.history(context.asset, 'close', context.sma_fast, '1d').mean()

slow_sma = data.history(context.asset, 'close', context.sma_slow, '1d').mean()

if fast_sma > slow_sma and context.portfolio.positions[context.asset].amount == 0:

order(context.asset, 100)

elif fast_sma < slow_sma and context.portfolio.positions[context.asset].amount > 0:

order(context.asset, -context.portfolio.positions[context.asset].amount)

record(fast=fast_sma, slow=slow_sma, price=data.current(context.asset, 'close'))

result = run_algorithm(

start=pd.Timestamp('2014-01-01', tz='utc'),

end=pd.Timestamp('2018-01-01', tz='utc'),

initialize=initialize,

handle_data=handle_data,

capital_base=100000,

data_frequency='daily',

bundle='quandl'

)

plt.figure(figsize=(12, 8))

plt.plot(result.portfolio_value)

plt.title('Portfolio Value')

plt.show()

TA-Lib

TA-Lib (Technical Analysis Library) là thư viện phân tích kỹ thuật nổi tiếng, cung cấp hơn 150 chỉ báo kỹ thuật và phương pháp xử lý tín hiệu.

import talib as ta

import numpy as np

close_prices = np.array(df['Close'])

high_prices = np.array(df['High'])

low_prices = np.array(df['Low'])

volume = np.array(df['Volume'])

sma = ta.SMA(close_prices, timeperiod=20)

ema = ta.EMA(close_prices, timeperiod=20)

rsi = ta.RSI(close_prices, timeperiod=14)

macd, macdsignal, macdhist = ta.MACD(close_prices, fastperiod=12, slowperiod=26, signalperiod=9)

upper, middle, lower = ta.BBANDS(close_prices, timeperiod=20, nbdevup=2, nbdevdn=2)

slowk, slowd = ta.STOCH(high_prices, low_prices, close_prices, fastk_period=5, slowk_period=3, slowk_matype=0, slowd_period=3, slowd_matype=0)

doji = ta.CDLDOJI(open_prices, high_prices, low_prices, close_prices)

engulfing = ta.CDLENGULFING(open_prices, high_prices, low_prices, close_prices)

hammer = ta.CDLHAMMER(open_prices, high_prices, low_prices, close_prices)

pyfolio

pyfolio là thư viện phân tích hiệu suất danh mục đầu tư từ Quantopian, cung cấp nhiều công cụ để đánh giá chiến lược.

import pyfolio as pf

returns = result.returns

pf.create_full_tear_sheet(returns)

pf.create_returns_tear_sheet(returns)

pf.create_position_tear_sheet(returns, result.positions)

pf.create_round_trip_tear_sheet(returns, result.positions, result.transactions)

pf.create_interesting_times_tear_sheet(returns)

vectorbt

vectorbt là thư viện phân tích và backtesting dựa trên NumPy với khả năng tính toán vector hóa mạnh mẽ.

import vectorbt as vbt

btc_price = vbt.YFData.download('BTC-USD').get('Close')

fast_ma = vbt.MA.run(btc_price, 10)

slow_ma = vbt.MA.run(btc_price, 50)

entries = fast_ma.ma_above(slow_ma)

exits = fast_ma.ma_below(slow_ma)

pf = vbt.Portfolio.from_signals(btc_price, entries, exits, init_cash=10000)

stats = pf.stats()

print(stats)

pf.plot().show()

4. Thư viện học máy và trí tuệ nhân tạo

Các thư viện này được sử dụng để xây dựng mô hình dự đoán và phân tích dữ liệu nâng cao.

scikit-learn

scikit-learn là thư viện học máy phổ biến nhất trong Python, cung cấp nhiều thuật toán cho phân loại, hồi quy, phân cụm, và giảm chiều.

from sklearn.ensemble import RandomForestClassifier

from sklearn.model_selection import train_test_split

from sklearn.metrics import accuracy_score

data = prepare_features(df)

X = data.drop('target', axis=1)

y = data['target']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

model = RandomForestClassifier(n_estimators=100, random_state=42)

model.fit(X_train, y_train)

y_pred = model.predict(X_test)

accuracy = accuracy_score(y_test, y_pred)

print(f"Độ chính xác: {accuracy:.2f}")

feature_importance = pd.DataFrame({

'feature': X.columns,

'importance': model.feature_importances_

}).sort_values('importance', ascending=False)

TensorFlow và Keras

TensorFlow là thư viện học sâu mạnh mẽ từ Google, trong khi Keras là API dễ sử dụng cho TensorFlow, chuyên cho xây dựng mạng neural.

import tensorflow as tf

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import Dense, LSTM, Dropout

from tensorflow.keras.optimizers import Adam

def create_sequences(data, seq_length):

xs, ys = [], []

for i in range(len(data) - seq_length - 1):

x = data[i:(i + seq_length)]

y = data[i + seq_length]

xs.append(x)

ys.append(y)

return np.array(xs), np.array(ys)

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler()

scaled_data = scaler.fit_transform(df[['Close']])

seq_length = 60

X, y = create_sequences(scaled_data, seq_length)

X = X.reshape(X.shape[0], X.shape[1], 1)

X_train, X_test = X[:-100], X[-100:]

y_train, y_test = y[:-100], y[-100:]

model = Sequential()

model.add(LSTM(50, return_sequences=True, input_shape=(seq_length, 1)))

model.add(Dropout(0.2))

model.add(LSTM(50, return_sequences=False))

model.add(Dropout(0.2))

model.add(Dense(1))

model.compile(optimizer=Adam(learning_rate=0.001), loss='mean_squared_error')

model.fit(X_train, y_train, epochs=20, batch_size=32, validation_split=0.1)

predictions = model.predict(X_test)

predictions = scaler.inverse_transform(predictions)

PyTorch

PyTorch là thư viện học sâu linh hoạt, được ưa chuộng trong cộng đồng nghiên cứu và phát triển.

import torch

import torch.nn as nn

import torch.optim as optim

from torch.utils.data import DataLoader, TensorDataset

X_train_tensor = torch.FloatTensor(X_train)

y_train_tensor = torch.FloatTensor(y_train).view(-1, 1)

train_dataset = TensorDataset(X_train_tensor, y_train_tensor)

train_loader = DataLoader(train_dataset, batch_size=32, shuffle=True)

class LSTMModel(nn.Module):

def __init__(self, input_size=1, hidden_size=50, num_layers=2, output_size=1):

super(LSTMModel, self).__init__()

self.hidden_size = hidden_size

self.num_layers = num_layers

self.lstm = nn.LSTM(input_size, hidden_size, num_layers, batch_first=True)

self.fc = nn.Linear(hidden_size, output_size)

def forward(self, x):

h0 = torch.zeros(self.num_layers, x.size(0), self.hidden_size).to(x.device)

c0 = torch.zeros(self.num_layers, x.size(0), self.hidden_size).to(x.device)

out, _ = self.lstm(x, (h0, c0))

out = self.fc(out[:, -1, :])

return out

model = LSTMModel()

criterion = nn.MSELoss()

optimizer = optim.Adam(model.parameters(), lr=0.001)

num_epochs = 20

for epoch in range(num_epochs):

for data, targets in train_loader:

optimizer.zero_grad()

outputs = model(data)

loss = criterion(outputs, targets)

loss.backward()

optimizer.step()

print(f"Epoch {epoch+1}/{num_epochs}, Loss: {loss.item():.4f}")

XGBoost

XGBoost là thư viện gradient boosting hiệu suất cao, được sử dụng rộng rãi trong các cuộc thi học máy và ứng dụng thực tế.

import xgboost as xgb

from sklearn.metrics import mean_squared_error

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

dtrain = xgb.DMatrix(X_train, label=y_train)

dtest = xgb.DMatrix(X_test, label=y_test)

params = {

'objective': 'reg:squarederror',

'max_depth': 6,

'alpha': 10,

'learning_rate': 0.1,

'n_estimators': 100

}

model = xgb.train(params, dtrain, num_boost_round=100)

y_pred = model.predict(dtest)

rmse = np.sqrt(mean_squared_error(y_test, y_pred))

print(f"RMSE: {rmse:.4f}")

importance = model.get_score(importance_type='gain')

sorted_importance = sorted(importance.items(), key=lambda x: x[1], reverse=True)

Prophet

Prophet là thư viện dự báo chuỗi thời gian từ Facebook, đặc biệt hiệu quả với dữ liệu có tính mùa vụ và nhiễu.

from prophet import Prophet

prophet_df = df.reset_index()[['Date', 'Close']].rename(columns={'Date': 'ds', 'Close': 'y'})

model = Prophet(daily_seasonality=True)

model.fit(prophet_df)

future = model.make_future_dataframe(periods=365)

forecast = model.predict(future)

print(forecast[['ds', 'yhat', 'yhat_lower', 'yhat_upper']].tail())

fig1 = model.plot(forecast)

fig2 = model.plot_components(forecast)

5. Thư viện trực quan hóa

Các thư viện giúp tạo biểu đồ và trực quan hóa dữ liệu tài chính.

Matplotlib

Matplotlib là thư viện trực quan hóa cơ bản và linh hoạt, nền tảng cho nhiều thư viện trực quan hóa khác.

import matplotlib.pyplot as plt

plt.figure(figsize=(14, 7))

plt.plot(df.index, df['Close'], label='Giá đóng cửa')

plt.plot(df.index, df['SMA_20'], label='SMA 20 ngày')

plt.plot(df.index, df['SMA_50'], label='SMA 50 ngày')

plt.title('Biểu đồ giá và đường trung bình động')

plt.xlabel('Ngày')

plt.ylabel('Giá ($)')

plt.legend()

plt.grid(True)

plt.show()

Plotly

Plotly cung cấp biểu đồ tương tác chất lượng cao, đặc biệt hữu ích cho dashboard và ứng dụng web.

import plotly.graph_objects as go

from plotly.subplots import make_subplots

fig = make_subplots(rows=2, cols=1, shared_xaxes=True,

vertical_spacing=0.1, subplot_titles=('Giá', 'Khối lượng'),

row_heights=[0.7, 0.3])

fig.add_trace(

go.Candlestick(

x=df.index,

open=df['Open'],

high=df['High'],

low=df['Low'],

close=df['Close'],

name='Giá'

),

row=1, col=1

)

fig.add_trace(

go.Scatter(

x=df.index,

y=df['SMA_20'],

name='SMA 20',

line=dict(color='blue', width=1)

),

row=1, col=1

)

fig.add_trace(

go.Bar(

x=df.index,

y=df['Volume'],

name='Khối lượng',

marker_color='rgba(0, 150, 0, 0.5)'

),

row=2, col=1

)

fig.update_layout(

title='Biểu đồ phân tích kỹ thuật',

yaxis_title='Giá ($)',

xaxis_title='Ngày',

height=800,

width=1200,

showlegend=True,

xaxis_rangeslider_visible=False

)

fig.show()

Seaborn

Seaborn xây dựng trên Matplotlib, cung cấp giao diện cấp cao để vẽ đồ thị thống kê đẹp mắt.

import seaborn as sns

plt.figure(figsize=(10, 6))

sns.histplot(df['Returns'].dropna(), kde=True, bins=50)

plt.title('Phân phối lợi nhuận hàng ngày')

plt.xlabel('Lợi nhuận (%)')

plt.axvline(x=0, color='r', linestyle='--')

plt.show()

plt.figure(figsize=(12, 10))

correlation = df[['Close', 'Volume', 'Returns', 'SMA_20', 'RSI']].corr()

sns.heatmap(correlation, annot=True, cmap='coolwarm', linewidths=0.5)

plt.title('Ma trận tương quan')

plt.show()

mplfinance

mplfinance là thư viện chuyên dụng để vẽ biểu đồ tài chính (kế thừa từ matplotlib.finance).

import mplfinance as mpf

mpf.plot(

df,

type='candle',

style='yahoo',

title='Biểu đồ phân tích kỹ thuật',

ylabel='Giá ($)',

volume=True,

mav=(20, 50),

figsize=(12, 8),

panel_ratios=(4, 1)

)

Bokeh

Bokeh là thư viện trực quan hóa tương tác, tập trung vào tương tác trong trình duyệt web.

from bokeh.plotting import figure, show, output_notebook

from bokeh.layouts import column

from bokeh.models import HoverTool, CrosshairTool, ColumnDataSource

source = ColumnDataSource(data=dict(

date=df.index,

open=df['Open'],

high=df['High'],

low=df['Low'],

close=df['Close'],

volume=df['Volume'],

sma20=df['SMA_20']

))

p1 = figure(x_axis_type="datetime", width=1200, height=500, title="Biểu đồ giá")

p1.line('date', 'sma20', source=source, line_width=2, color='blue', legend_label='SMA 20')

p1.segment('date', 'high', 'date', 'low', source=source, color="black")

p1.rect('date', x_range=0.5, width=0.8, height='open', fill_color="green", line_color="black",

fill_alpha=0.5, source=source)

hover = HoverTool()

hover.tooltips = [

("Ngày", "@date{%F}"),

("Mở", "@open{0.2f}"),

("Cao", "@high{0.2f}"),

("Thấp", "@low{0.2f}"),

("Đóng", "@close{0.2f}")

]

hover.formatters = {"@date": "datetime"}

p1.add_tools(hover)

p2 = figure(x_axis_type="datetime", width=1200, height=200, x_range=p1.x_range)

p2.vbar('date', 0.8, 'volume', source=source, color="navy", alpha=0.5)

p2.yaxis.axis_label = "Khối lượng"

show(column(p1, p2))

Altair

Altair là thư viện trực quan hóa khai báo dựa trên Vega-Lite, cho phép tạo biểu đồ phức tạp với cú pháp đơn giản.

import altair as alt

base = alt.Chart(df.reset_index()).encode(

x='Date:T',

tooltip=['Date:T', 'Open:Q', 'High:Q', 'Low:Q', 'Close:Q', 'Volume:Q']

)

line = base.mark_line().encode(

y='Close:Q',

color=alt.value('blue')

)

sma = base.mark_line().encode(

y='SMA_20:Q',

color=alt.value('red')

)

volume = base.mark_bar().encode(

y='Volume:Q',

color=alt.value('gray')

).properties(

height=100

)

chart = alt.vconcat(

(line + sma).properties(title='Giá và SMA'),

volume.properties(title='Khối lượng')

).properties(

width=800

)

chart

Kết luận

Python cung cấp một hệ sinh thái phong phú các thư viện chuyên dụng cho giao dịch định lượng, từ phân tích dữ liệu cơ bản đến xây dựng mô hình học máy phức tạp. Những thư viện này đã biến Python thành ngôn ngữ hàng đầu trong lĩnh vực tài chính định lượng, cho phép các nhà giao dịch và nhà phát triển nhanh chóng triển khai từ ý tưởng đến chiến lược giao dịch.

Tùy thuộc vào nhu cầu cụ thể, bạn có thể kết hợp các thư viện khác nhau để tạo ra một quy trình giao dịch hoàn chỉnh - từ thu thập dữ liệu, phân tích, huấn luyện mô hình, backtesting, đến giao dịch thực tế. Việc liên tục cập nhật kiến thức về các thư viện này sẽ giúp bạn tận dụng tối đa sức mạnh của Python trong giao dịch định lượng.