📊 Phân Tích Rủi Ro và Lợi Nhuận Danh Mục Đầu Tư (Portfolio)

📊 Phân Tích Rủi Ro và Lợi Nhuận Danh Mục Đầu Tư (Portfolio) với Python

Giới thiệu

Quản lý danh mục đầu tư (portfolio) hiệu quả đòi hỏi sự cân bằng giữa rủi ro và lợi nhuận kỳ vọng. Trong bài viết này, chúng ta sẽ tìm hiểu cách sử dụng Python để phân tích, đánh giá và tối ưu hóa danh mục đầu tư chứng khoán, từ việc thu thập dữ liệu, tính toán các chỉ số rủi ro-lợi nhuận, cho đến việc áp dụng lý thuyết danh mục đầu tư hiện đại (Modern Portfolio Theory) của Harry Markowitz.

Những công cụ cần thiết

# Thư viện cần cài đặt

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import yfinance as yf

import scipy.optimize as sco

from scipy import stats

import cvxpy as cp

import warnings

# Thiết lập hiển thị

warnings.filterwarnings('ignore')

plt.style.use('fivethirtyeight')

np.random.seed(777)

Thu thập dữ liệu

Sử dụng Yahoo Finance API

Bước đầu tiên trong phân tích danh mục đầu tư là thu thập dữ liệu lịch sử. Chúng ta sẽ sử dụng thư viện yfinance để tải dữ liệu từ Yahoo Finance:

def get_stock_data(tickers, start_date, end_date, interval='1d'):

"""

Thu thập dữ liệu cổ phiếu từ Yahoo Finance

Tham số:

tickers (list): Danh sách mã cổ phiếu

start_date (str): Ngày bắt đầu (YYYY-MM-DD)

end_date (str): Ngày kết thúc (YYYY-MM-DD)

interval (str): Khoảng thời gian ('1d', '1wk', '1mo')

Trả về:

pd.DataFrame: DataFrame chứa giá đóng cửa đã điều chỉnh của các cổ phiếu

"""

data = yf.download(tickers, start=start_date, end=end_date, interval=interval)['Adj Close']

# Xử lý trường hợp chỉ có một mã cổ phiếu

if isinstance(data, pd.Series):

data = pd.DataFrame(data)

data.columns = [tickers]

# Kiểm tra và xử lý dữ liệu thiếu

if data.isnull().sum().sum() > 0:

print(f"Có {data.isnull().sum().sum()} giá trị thiếu. Tiến hành điền giá trị thiếu...")

data = data.fillna(method='ffill').fillna(method='bfill')

return data

Ví dụ thu thập dữ liệu cho một số cổ phiếu

# Danh sách các mã cổ phiếu mẫu (đổi thành các mã trên HOSE nếu cần)

tickers = ['AAPL', 'MSFT', 'GOOG', 'AMZN', 'META', 'TSLA', 'NVDA', 'JPM', 'V', 'PG']

# Khoảng thời gian

start_date = '2018-01-01'

end_date = '2023-01-01'

# Thu thập dữ liệu

prices = get_stock_data(tickers, start_date, end_date)

print(prices.head())

# Vẽ biểu đồ giá cổ phiếu (chuẩn hóa)

normalized_prices = prices / prices.iloc[0] * 100

plt.figure(figsize=(12, 8))

normalized_prices.plot()

plt.title('Diễn biến giá cổ phiếu (chuẩn hóa)')

plt.xlabel('Ngày')

plt.ylabel('Giá chuẩn hóa (100 = giá ban đầu)')

plt.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

Tính toán lợi nhuận

Tính lợi nhuận hàng ngày và thống kê mô tả

def calculate_returns(prices, period='daily'):

"""

Tính lợi nhuận của cổ phiếu

Tham số:

prices (pd.DataFrame): DataFrame chứa giá cổ phiếu

period (str): Kỳ hạn lợi nhuận ('daily', 'weekly', 'monthly', 'annual')

Trả về:

pd.DataFrame: DataFrame chứa lợi nhuận

"""

if period == 'daily':

returns = prices.pct_change().dropna()

elif period == 'weekly':

returns = prices.resample('W').last().pct_change().dropna()

elif period == 'monthly':

returns = prices.resample('M').last().pct_change().dropna()

elif period == 'annual':

returns = prices.resample('Y').last().pct_change().dropna()

else:

raise ValueError("Kỳ hạn không hợp lệ. Sử dụng 'daily', 'weekly', 'monthly', hoặc 'annual'")

return returns

# Tính lợi nhuận hàng ngày

daily_returns = calculate_returns(prices)

# Thống kê mô tả

desc_stats = daily_returns.describe().T

desc_stats['annualized_return'] = daily_returns.mean() * 252

desc_stats['annualized_vol'] = daily_returns.std() * np.sqrt(252)

desc_stats['sharpe_ratio'] = desc_stats['annualized_return'] / desc_stats['annualized_vol']

print(desc_stats[['mean', 'std', 'annualized_return', 'annualized_vol', 'sharpe_ratio']])

Biểu đồ phân phối lợi nhuận

def plot_returns_distribution(returns):

"""

Vẽ biểu đồ phân phối lợi nhuận

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

"""

plt.figure(figsize=(15, 10))

for i, ticker in enumerate(returns.columns):

plt.subplot(3, 4, i+1)

# Histogram

sns.histplot(returns[ticker], kde=True, stat="density", linewidth=0)

# Normal distribution curve

xmin, xmax = plt.xlim()

x = np.linspace(xmin, xmax, 100)

p = stats.norm.pdf(x, returns[ticker].mean(), returns[ticker].std())

plt.plot(x, p, 'k', linewidth=2)

plt.title(f'Phân phối lợi nhuận {ticker}')

plt.xlabel('Lợi nhuận hàng ngày')

plt.ylabel('Mật độ')

plt.tight_layout()

Phân tích rủi ro

Tính toán các thước đo rủi ro

def calculate_risk_metrics(returns, risk_free_rate=0.0):

"""

Tính toán các thước đo rủi ro cho từng cổ phiếu

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

risk_free_rate (float): Lãi suất phi rủi ro (annualized)

Trả về:

pd.DataFrame: DataFrame chứa các thước đo rủi ro

"""

# Chuyển đổi lãi suất phi rủi ro sang tỷ lệ hàng ngày

daily_rf = (1 + risk_free_rate) ** (1/252) - 1

# DataFrame để lưu kết quả

metrics = pd.DataFrame(index=returns.columns)

# Độ biến động (Volatility) hàng năm

metrics['volatility'] = returns.std() * np.sqrt(252)

# Tỷ lệ Sharpe

excess_returns = returns.sub(daily_rf, axis=0)

metrics['sharpe_ratio'] = (excess_returns.mean() * 252) / metrics['volatility']

# Maximum Drawdown

cumulative_returns = (1 + returns).cumprod()

rolling_max = cumulative_returns.cummax()

drawdown = (cumulative_returns - rolling_max) / rolling_max

metrics['max_drawdown'] = drawdown.min()

# Value at Risk (VaR) 95%

metrics['var_95'] = returns.quantile(0.05)

# Conditional Value at Risk (CVaR) 95%

metrics['cvar_95'] = returns[returns < returns.quantile(0.05)].mean()

# Tỷ lệ Sortino

negative_returns = returns.copy()

negative_returns[negative_returns > 0] = 0

downside_deviation = negative_returns.std() * np.sqrt(252)

metrics['sortino_ratio'] = (excess_returns.mean() * 252) / downside_deviation

# Beta (so với chỉ số S&P 500)

sp500 = yf.download('^GSPC', start=returns.index[0], end=returns.index[-1], interval='1d')['Adj Close']

sp500_returns = sp500.pct_change().dropna()

# Chỉ lấy những ngày trùng khớp

common_index = returns.index.intersection(sp500_returns.index)

returns_aligned = returns.loc[common_index]

sp500_returns_aligned = sp500_returns.loc[common_index]

# Tính beta

for ticker in returns.columns:

covariance = np.cov(returns_aligned[ticker], sp500_returns_aligned)[0, 1]

variance = np.var(sp500_returns_aligned)

metrics.loc[ticker, 'beta'] = covariance / variance

return metrics

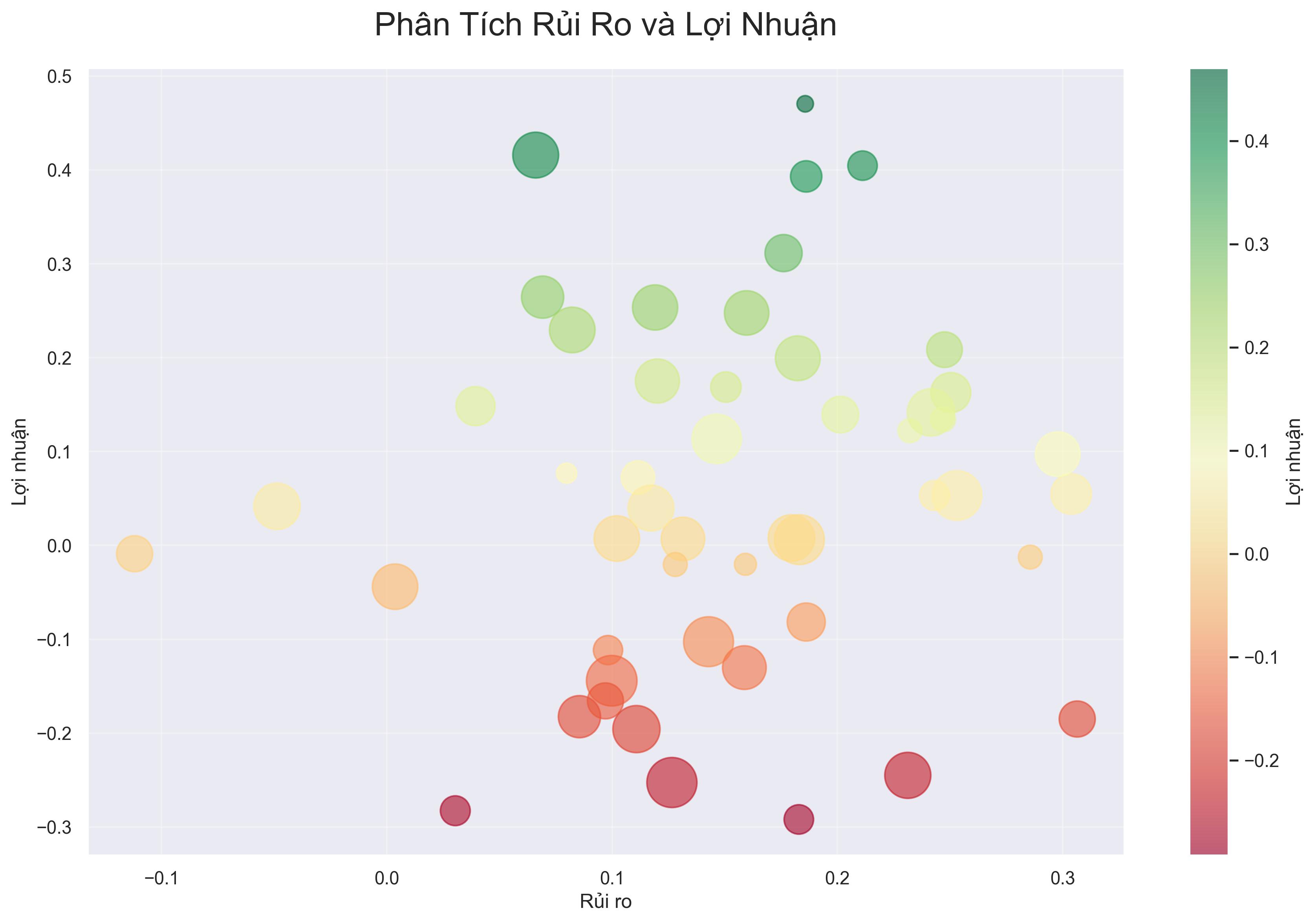

Vẽ biểu đồ rủi ro-lợi nhuận

def plot_risk_return(returns, risk_metrics, period=252):

"""

Vẽ biểu đồ rủi ro-lợi nhuận

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

risk_metrics (pd.DataFrame): DataFrame chứa các thước đo rủi ro

period (int): Số ngày trong một năm để annualize lợi nhuận

"""

plt.figure(figsize=(12, 8))

# Tính lợi nhuận trung bình hàng năm

annual_returns = returns.mean() * period

# Biểu đồ scatter

plt.scatter(risk_metrics['volatility'], annual_returns, s=200, alpha=0.6)

# Thêm nhãn

for i, ticker in enumerate(returns.columns):

plt.annotate(ticker,

(risk_metrics['volatility'][i], annual_returns[i]),

xytext=(10, 5),

textcoords='offset points',

fontsize=12)

# Thêm title và label

plt.title('Biểu đồ Rủi ro - Lợi nhuận', fontsize=16)

plt.xlabel('Rủi ro (Độ biến động hàng năm)', fontsize=14)

plt.ylabel('Lợi nhuận kỳ vọng hàng năm', fontsize=14)

# Thêm đường Linear Regression

z = np.polyfit(risk_metrics['volatility'], annual_returns, 1)

p = np.poly1d(z)

plt.plot(risk_metrics['volatility'], p(risk_metrics['volatility']), "r--", linewidth=2)

plt.tight_layout()

Vẽ biểu đồ Drawdown

def plot_drawdown(returns):

"""

Vẽ biểu đồ drawdown cho từng cổ phiếu

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

"""

plt.figure(figsize=(12, 8))

for ticker in returns.columns:

# Tính cumulative returns

cumulative_returns = (1 + returns[ticker]).cumprod()

# Tính rolling maximum

rolling_max = cumulative_returns.cummax()

# Tính drawdown

drawdown = (cumulative_returns - rolling_max) / rolling_max

# Vẽ drawdown

plt.plot(drawdown, label=ticker)

plt.title('Biểu đồ Drawdown', fontsize=16)

plt.xlabel('Ngày', fontsize=14)

plt.ylabel('Drawdown', fontsize=14)

plt.legend(bbox_to_anchor=(1.05, 1), loc='upper left')

plt.tight_layout()

Ma trận tương quan và phân tích đa dạng hóa

Tính ma trận tương quan và hiển thị heatmap

def plot_correlation_matrix(returns):

"""

Vẽ ma trận tương quan giữa các cổ phiếu

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

"""

# Tính ma trận tương quan

corr_matrix = returns.corr()

# Thiết lập kích thước biểu đồ

plt.figure(figsize=(10, 8))

# Vẽ heatmap

cmap = sns.diverging_palette(220, 10, as_cmap=True)

sns.heatmap(corr_matrix, annot=True, cmap=cmap, center=0,

square=True, linewidths=.5, cbar_kws={"shrink": .8})

plt.title('Ma trận tương quan giữa các cổ phiếu', fontsize=16)

plt.tight_layout()

Phân tích đa dạng hóa danh mục

def calculate_portfolio_performance(weights, returns):

"""

Tính toán hiệu suất của danh mục đầu tư

Tham số:

weights (np.array): Trọng số phân bổ cho từng cổ phiếu

returns (pd.DataFrame): DataFrame chứa lợi nhuận

Trả về:

tuple: (lợi nhuận kỳ vọng, độ biến động, tỷ lệ Sharpe)

"""

# Lợi nhuận danh mục

portfolio_return = np.sum(returns.mean() * weights) * 252

# Độ biến động danh mục

portfolio_volatility = np.sqrt(np.dot(weights.T, np.dot(returns.cov() * 252, weights)))

# Tỷ lệ Sharpe

sharpe_ratio = portfolio_return / portfolio_volatility

return portfolio_return, portfolio_volatility, sharpe_ratio

Phân tích hiệu quả đa dạng hóa ngẫu nhiên

def random_portfolios(returns, num_portfolios=10000):

"""

Tạo ngẫu nhiên các danh mục đầu tư và tính hiệu suất

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

num_portfolios (int): Số lượng danh mục ngẫu nhiên cần tạo

Trả về:

tuple: (results, weights) - kết quả hiệu suất và trọng số tương ứng

"""

results = np.zeros((num_portfolios, 3))

weights_record = np.zeros((num_portfolios, len(returns.columns)))

for i in range(num_portfolios):

# Tạo trọng số ngẫu nhiên

weights = np.random.random(len(returns.columns))

weights /= np.sum(weights)

weights_record[i, :] = weights

# Tính hiệu suất

results[i, 0], results[i, 1], results[i, 2] = calculate_portfolio_performance(weights, returns)

return results, weights_record

Vẽ biểu đồ đường biên hiệu quả (Efficient Frontier)

def plot_efficient_frontier(returns, results, weights_record):

"""

Vẽ biểu đồ đường biên hiệu quả

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

results (np.array): Mảng kết quả hiệu suất của các danh mục ngẫu nhiên

weights_record (np.array): Mảng trọng số của các danh mục ngẫu nhiên

"""

plt.figure(figsize=(12, 8))

# Vẽ các danh mục ngẫu nhiên

plt.scatter(results[:, 1], results[:, 0], c=results[:, 2],

cmap='viridis', marker='o', s=10, alpha=0.3)

# Đánh dấu danh mục có Sharpe ratio cao nhất

max_sharpe_idx = np.argmax(results[:, 2])

max_sharpe_portfolio = results[max_sharpe_idx]

plt.scatter(max_sharpe_portfolio[1], max_sharpe_portfolio[0],

marker='*', color='r', s=500, label='Danh mục tối ưu theo Sharpe')

# Đánh dấu danh mục có độ biến động thấp nhất

min_vol_idx = np.argmin(results[:, 1])

min_vol_portfolio = results[min_vol_idx]

plt.scatter(min_vol_portfolio[1], min_vol_portfolio[0],

marker='*', color='g', s=500, label='Danh mục có độ biến động thấp nhất')

# Đánh dấu cổ phiếu riêng lẻ

for i, ticker in enumerate(returns.columns):

individual_return = returns.mean()[i] * 252

individual_volatility = returns.std()[i] * np.sqrt(252)

plt.scatter(individual_volatility, individual_return, marker='o', s=200,

color='black', label=ticker if i == 0 else "")

plt.annotate(ticker, (individual_volatility, individual_return),

xytext=(10, 5), textcoords='offset points')

# Thêm title và label

plt.colorbar(label='Sharpe ratio')

plt.title('Đường biên hiệu quả (Efficient Frontier)', fontsize=16)

plt.xlabel('Độ biến động (Rủi ro)', fontsize=14)

plt.ylabel('Lợi nhuận kỳ vọng', fontsize=14)

plt.legend()

# Hiển thị thông tin về danh mục tối ưu

print("Danh mục tối ưu theo tỷ lệ Sharpe:")

print(f"Lợi nhuận kỳ vọng: {max_sharpe_portfolio[0]:.4f}")

print(f"Độ biến động: {max_sharpe_portfolio[1]:.4f}")

print(f"Tỷ lệ Sharpe: {max_sharpe_portfolio[2]:.4f}")

print("\nPhân bổ vốn:")

for i, ticker in enumerate(returns.columns):

print(f"{ticker}: {weights_record[max_sharpe_idx, i] * 100:.2f}%")

plt.tight_layout()

Tối ưu hóa danh mục đầu tư

Tìm danh mục tối ưu theo lý thuyết Markowitz

def optimize_portfolio(returns, risk_free_rate=0.0, target_return=None):

"""

Tìm danh mục đầu tư tối ưu sử dụng lý thuyết Markowitz

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

risk_free_rate (float): Lãi suất phi rủi ro (annualized)

target_return (float): Lợi nhuận mục tiêu (annualized), nếu None thì tối đa hóa Sharpe ratio

Trả về:

tuple: (optimal_weights, expected_return, volatility, sharpe_ratio)

"""

n = len(returns.columns)

returns_mean = returns.mean() * 252

cov_matrix = returns.cov() * 252

# Khai báo biến

w = cp.Variable(n)

# Khai báo hàm mục tiêu

if target_return is None:

# Tối đa hóa tỷ lệ Sharpe

risk = cp.quad_form(w, cov_matrix)

ret = returns_mean @ w

sharpe = (ret - risk_free_rate) / cp.sqrt(risk)

objective = cp.Maximize(sharpe)

else:

# Tối thiểu hóa rủi ro với lợi nhuận mục tiêu

risk = cp.quad_form(w, cov_matrix)

objective = cp.Minimize(risk)

# Ràng buộc

constraints = [

cp.sum(w) == 1, # Tổng trọng số bằng 1

w >= 0 # Không cho phép bán khống

]

# Thêm ràng buộc về lợi nhuận mục tiêu nếu cần

if target_return is not None:

constraints.append(returns_mean @ w >= target_return)

# Giải bài toán tối ưu

problem = cp.Problem(objective, constraints)

problem.solve()

# Lấy kết quả

optimal_weights = w.value

expected_return = returns_mean.dot(optimal_weights)

volatility = np.sqrt(optimal_weights.T @ cov_matrix @ optimal_weights)

sharpe_ratio = (expected_return - risk_free_rate) / volatility

return optimal_weights, expected_return, volatility, sharpe_ratio

Vẽ đường biên hiệu quả lý thuyết

def plot_theoretical_efficient_frontier(returns, risk_free_rate=0.0, points=100):

"""

Vẽ đường biên hiệu quả lý thuyết

Tham số:

returns (pd.DataFrame): DataFrame chứa lợi nhuận

risk_free_rate (float): Lãi suất phi rủi ro (annualized)

points (int): Số điểm để vẽ đường biên hiệu quả

"""

plt.figure(figsize=(12, 8))

# Tính danh mục có độ biến động thấp nhất

min_vol_weights, min_vol_return, min_vol_risk, _ = optimize_portfolio(returns, risk_free_rate, target_return=None)

# Tính danh mục có tỷ lệ Sharpe cao nhất

max_sharpe_weights, max_sharpe_return, max_sharpe_risk, max_sharpe = optimize_portfolio(returns, risk_free_rate)

# Tính các danh mục tối ưu với lợi nhuận mục tiêu khác nhau

target_returns = np.linspace(min_vol_return, max(returns.mean()) * 252 * 1.2, points)

efficient_risk = []

efficient_return = []

for target in target_returns:

try:

weights, ret, risk, _ = optimize_portfolio(returns, risk_free_rate, target_return=target)

efficient_risk.append(risk)

efficient_return.append(ret)

except:

pass

# Vẽ đường biên hiệu quả

plt.plot(efficient_risk, efficient_return, 'b-', linewidth=3, label='Đường biên hiệu quả')

# Đánh dấu danh mục có độ biến động thấp nhất

plt.scatter(min_vol_risk, min_vol_return, marker='*', color='g', s=500,

label='Danh mục có độ biến động thấp nhất')

# Đánh dấu danh mục có tỷ lệ Sharpe cao nhất

plt.scatter(max_sharpe_risk, max_sharpe_return, marker='*', color='r', s=500,

label='Danh mục tối ưu theo Sharpe')

# Vẽ đường CML (Capital Market Line)

x_cml = np.linspace(0, max(efficient_risk) * 1.2, 100)

y_cml = risk_free_rate + x_cml * (max_sharpe_return - risk_free_rate) / max_sharpe_risk

plt.plot(x_cml, y_cml, 'r--', label='CML')

# Đánh dấu cổ phiếu riêng lẻ

for i, ticker in enumerate(returns.columns):

individual_return = returns.mean()[i] * 252

individual_volatility = returns.std()[i] * np.sqrt(252)

plt.scatter(individual_volatility, individual_return, marker='o', s=200,

color='black')

plt.annotate(ticker, (individual_volatility, individual_return),

xytext=(10, 5), textcoords='offset points')

# Thêm title và label

plt.title('Đường biên hiệu quả lý thuyết', fontsize=16)

plt.xlabel('Độ biến động (Rủi ro)', fontsize=14)

plt.ylabel('Lợi nhuận kỳ vọng', fontsize=14)

plt.legend()

# Hiển thị thông tin về danh mục tối ưu

print("Danh mục tối ưu theo tỷ lệ Sharpe:")

print(f"Lợi nhuận kỳ vọng: {max_sharpe_return:.4f}")

print(f"Độ biến động: {max_sharpe_risk:.4f}")

print(f"Tỷ lệ Sharpe: {max_sharpe:.4f}")

print("\nPhân bổ vốn:")

for i, ticker in enumerate(returns.columns):

print(f"{ticker}: {max_sharpe_weights[i] * 100:.2f}%")

plt.tight_layout()

Đánh giá hiệu suất danh mục đầu tư trong quá khứ

Mô phỏng hiệu suất danh mục theo thời gian

def simulate_portfolio_performance(weights, prices):

"""

Mô phỏng hiệu suất danh mục theo thời gian

Tham số:

weights (np.array): Trọng số phân bổ cho từng cổ phiếu

prices (pd.DataFrame): DataFrame chứa giá cổ phiếu

Trả về:

pd.Series: Series chứa giá trị danh mục theo thời gian

"""

# Chuẩn hóa giá

normalized_prices = prices / prices.iloc[0]

# Tính giá trị danh mục

portfolio_value = (normalized_prices * weights).sum(axis=1)

return portfolio_value

So sánh hiệu suất với chỉ số thị trường

def compare_with_benchmark(portfolio_value, start_date, end_date, benchmark='^GSPC'):

"""

So sánh hiệu suất của danh mục với chỉ số thị trường

Tham số:

portfolio_value (pd.Series): Series chứa giá trị danh mục

start_date (str): Ngày bắt đầu (YYYY-MM-DD)

end_date (str): Ngày kết thúc (YYYY-MM-DD)

benchmark (str): Mã chỉ số thị trường (mặc định là S&P 500)

Trả về:

tuple: (portfolio_return, benchmark_return)

"""

# Tải dữ liệu chỉ số

benchmark_data = yf.download(benchmark, start=start_date, end=end_date)['Adj Close']

# Chuẩn hóa giá trị

normalized_benchmark = benchmark_data / benchmark_data.iloc[0]

normalized_portfolio = portfolio_value / portfolio_value.iloc[0]

# Vẽ biểu đồ

plt.figure(figsize=(12, 8))

plt.plot(normalized_portfolio, label='Danh mục của bạn')

plt.plot(normalized_benchmark, label=f'Chỉ số {benchmark}')

plt.title('So sánh hiệu suất với chỉ số thị trường', fontsize=16)

plt.xlabel('Ngày', fontsize=14)

plt.ylabel('Giá trị (chuẩn hóa)', fontsize=14)

plt.legend()

plt.grid(True, alpha=0.3)

# Tính toán lợi nhuận tổng thể

portfolio_return = normalized_portfolio.iloc[-1] - 1

benchmark_return = normalized_benchmark.iloc[-1] - 1

# Thông tin về alpha và beta

portfolio_returns = normalized_portfolio.pct_change().dropna()

benchmark_returns = normalized_benchmark.pct_change().dropna()

# Chỉ lấy những ngày trùng khớp

common_index = portfolio_returns.index.intersection(benchmark_returns.index)

portfolio_returns = portfolio_returns.loc[common_index]

benchmark_returns = benchmark_returns.loc[common_index]

# Tính beta

covariance = np.cov(portfolio_returns, benchmark_returns)[0, 1]

variance = np.var(benchmark_returns)

beta = covariance / variance

# Tính alpha (Jensen's Alpha)

risk_free_rate = 0.0 # Có thể thay đổi tùy vào lãi suất thực tế

expected_return = risk_free_rate + beta * (benchmark_returns.mean() * 252 - risk_free_rate)

alpha = portfolio_returns.mean() * 252 - expected_return

print(f"Lợi nhuận danh mục: {portfolio_return:.4f} ({portfolio_return * 100:.2f}%)")

print(f"Lợi nhuận chỉ số {benchmark}: {benchmark_return:.4f} ({benchmark_return * 100:.2f}%)")

print(f"Alpha: {alpha:.4f}")

print(f"Beta: {beta:.4f}")

plt.tight_layout()

return portfolio_return, benchmark_return

Kiểm định sức chịu đựng (Stress Testing)

Phân tích kịch bản (Scenario Analysis)

def stress_test_scenarios(weights, returns, scenarios):

"""

Phân tích kịch bản stress test

Tham số:

weights (np.array): Trọng số phân bổ cho từng cổ phiếu

returns (pd.DataFrame): DataFrame chứa lợi nhuận

scenarios (dict): Dictionary chứa các kịch bản stress test

{'tên kịch bản': [start_date, end_date]}

Trả về:

pd.DataFrame: DataFrame chứa kết quả stress test

"""

results = pd.DataFrame(columns=['scenario', 'portfolio_return', 'max_drawdown'])

for scenario_name, (start_date, end_date) in scenarios.items():

# Lấy dữ liệu theo kịch bản

scenario_data = returns.loc[start_date:end_date]

# Tính lợi nhuận danh mục trong kịch bản

portfolio_returns = (scenario_data * weights).sum(axis=1)

# Tính cumulative returns

cumulative_returns = (1 + portfolio_returns).cumprod()

# Tính max drawdown

rolling_max = cumulative_returns.cummax()

drawdown = (cumulative_returns - rolling_max) / rolling_max

max_drawdown = drawdown.min()

# Tính tổng lợi nhuận

total_return = (1 + portfolio_returns).prod() - 1

results = results.append({

'scenario': scenario_name,

'portfolio_return': total_return,

'max_drawdown': max_drawdown

}, ignore_index=True)

return results

Phân tích Monte Carlo

def monte_carlo_simulation(weights, returns, n_simulations=1000, time_horizon=252):

"""

Thực hiện mô phỏng Monte Carlo cho danh mục đầu tư

Tham số:

weights (np.array): Trọng số phân bổ cho từng cổ phiếu

returns (pd.DataFrame): DataFrame chứa lợi nhuận

n_simulations (int): Số lần mô phỏng

time_horizon (int): Khoảng thời gian mô phỏng (ngày giao dịch)

Trả về:

np.array: Mảng kết quả mô phỏng

"""

# Tính mean và covariance matrix

mean_returns = returns.mean()

cov_matrix = returns.cov()

# Tính lợi nhuận danh mục

portfolio_mean = np.sum(mean_returns * weights)

portfolio_var = np.dot(weights.T, np.dot(cov_matrix, weights))

portfolio_std = np.sqrt(portfolio_var)

# Mô phỏng

simulations = np.zeros((n_simulations, time_horizon))

for i in range(n_simulations):

# Tạo chuỗi lợi nhuận ngẫu nhiên

Z = np.random.normal(portfolio_mean, portfolio_std, time_horizon)

# Tính cumulative returns

simulations[i] = np.cumprod(1 + Z) - 1

# Vẽ biểu đồ

plt.figure(figsize=(12, 8))

for i in range(n_simulations):

plt.plot(simulations[i], linewidth=0.5, alpha=0.1, color='blue')

# Tính các phân vị

percentiles = [10, 50, 90]

percentile_data = np.percentile(simulations, percentiles, axis=0)

for i, p in enumerate(percentiles):

plt.plot(percentile_data[i], linewidth=2,

label=f'Phân vị thứ {p}',

color='red' if p == 50 else 'black')

plt.title('Mô phỏng Monte Carlo', fontsize=16)

plt.xlabel('Ngày', fontsize=14)

plt.ylabel('Lợi nhuận tích lũy', fontsize=14)

plt.legend()

plt.grid(True, alpha=0.3)

# Tính kết quả

final_returns = simulations[:, -1]

print(f"Lợi nhuận kỳ vọng sau {time_horizon} ngày: {np.mean(final_returns):.4f} ({np.mean(final_returns) * 100:.2f}%)")

print(f"VaR (95%): {np.percentile(final_returns, 5):.4f} ({np.percentile(final_returns, 5) * 100:.2f}%)")

print(f"VaR (99%): {np.percentile(final_returns, 1):.4f} ({np.percentile(final_returns, 1) * 100:.2f}%)")

plt.tight_layout()

return simulations

Tái cân bằng danh mục đầu tư

Mô phỏng tái cân bằng định kỳ

def simulate_rebalancing(weights, prices, rebalance_frequency='M'):

"""

Mô phỏng hiệu suất danh mục với tái cân bằng định kỳ

Tham số:

weights (np.array): Trọng số ban đầu cho từng cổ phiếu

prices (pd.DataFrame): DataFrame chứa giá cổ phiếu

rebalance_frequency (str): Tần suất tái cân bằng ('D', 'W', 'M', 'Q', 'Y')

Trả về:

tuple: (rebalanced_portfolio, buy_hold_portfolio) - hiệu suất danh mục tái cân bằng và mua giữ

"""

# Ban đầu giả sử có 1 đơn vị tiền

initial_investment = 1.0

# Tính số lượng cổ phiếu ban đầu

initial_prices = prices.iloc[0]

shares = np.array(weights) * initial_investment / initial_prices

# Khởi tạo các biến theo dõi

portfolio_value = pd.Series(index=prices.index)

buy_hold_value = pd.Series(index=prices.index)

# Tính giá trị danh mục theo thời gian

for date in prices.index:

# Giá trị hiện tại của danh mục

current_value = np.sum(shares * prices.loc[date])

portfolio_value[date] = current_value

# Nếu là ngày cần tái cân bằng và không phải ngày đầu tiên

if date != prices.index[0]:

if rebalance_frequency == 'D':

rebalance = True

elif rebalance_frequency == 'W' and date.dayofweek == 0: # Thứ 2

rebalance = True

elif rebalance_frequency == 'M' and date.day == 1: # Ngày đầu tháng

rebalance = True

elif rebalance_frequency == 'Q' and date.month in [1, 4, 7, 10] and date.day == 1:

rebalance = True

elif rebalance_frequency == 'Y' and date.month == 1 and date.day == 1:

rebalance = True

else:

rebalance = False

if rebalance:

# Tính trọng số hiện tại

current_weights = shares * prices.loc[date] / current_value

# Nếu chênh lệch đáng kể so với trọng số mục tiêu, thực hiện tái cân bằng

if np.max(np.abs(current_weights - weights)) > 0.01: # 1% threshold

# Tái cân bằng

shares = np.array(weights) * current_value / prices.loc[date]

# Mô phỏng danh mục mua và giữ (không tái cân bằng)

buy_hold = (prices / prices.iloc[0] * weights).sum(axis=1)

# Vẽ biểu đồ so sánh

plt.figure(figsize=(12, 8))

plt.plot(portfolio_value / portfolio_value.iloc[0], label=f'Danh mục tái cân bằng ({rebalance_frequency})')

plt.plot(buy_hold, label='Danh mục mua và giữ')

plt.title('So sánh hiệu suất: Tái cân bằng vs Mua và giữ', fontsize=16)

plt.xlabel('Ngày', fontsize=14)

plt.ylabel('Giá trị (chuẩn hóa)', fontsize=14)

plt.legend()

plt.grid(True, alpha=0.3)

# Tính toán lợi nhuận tổng thể

rebalance_return = portfolio_value.iloc[-1] / portfolio_value.iloc[0] - 1

buy_hold_return = buy_hold.iloc[-1] - 1

print(f"Lợi nhuận danh mục tái cân bằng: {rebalance_return:.4f} ({rebalance_return * 100:.2f}%)")

print(f"Lợi nhuận danh mục mua và giữ: {buy_hold_return:.4f} ({buy_hold_return * 100:.2f}%)")

plt.tight_layout()

return portfolio_value / portfolio_value.iloc[0], buy_hold

Ứng dụng thực tế

Ví dụ tổng hợp phân tích danh mục đầu tư

def complete_portfolio_analysis(tickers, start_date, end_date):

"""

Thực hiện phân tích danh mục đầu tư toàn diện

Tham số:

tickers (list): Danh sách mã cổ phiếu

start_date (str): Ngày bắt đầu (YYYY-MM-DD)

end_date (str): Ngày kết thúc (YYYY-MM-DD)

Trả về:

dict: Dictionary chứa thông tin về danh mục tối ưu

"""

# Thu thập dữ liệu

prices = get_stock_data(tickers, start_date, end_date)

returns = calculate_returns(prices)

# Tính toán các thước đo rủi ro

risk_metrics = calculate_risk_metrics(returns)

# Vẽ biểu đồ rủi ro-lợi nhuận

plot_risk_return(returns, risk_metrics)

# Vẽ ma trận tương quan

plot_correlation_matrix(returns)

# Tìm danh mục tối ưu

optimal_weights, expected_return, volatility, sharpe_ratio = optimize_portfolio(returns)

# Vẽ đường biên hiệu quả lý thuyết

plot_theoretical_efficient_frontier(returns)

# Mô phỏng hiệu suất danh mục

portfolio_value = simulate_portfolio_performance(optimal_weights, prices)

# So sánh với chỉ số thị trường

compare_with_benchmark(portfolio_value, start_date, end_date)

# Mô phỏng tái cân bằng

simulate_rebalancing(optimal_weights, prices, rebalance_frequency='M')

# Mô phỏng Monte Carlo

monte_carlo_simulation(optimal_weights, returns)

# Kết quả

result = {

'optimal_weights': dict(zip(tickers, optimal_weights)),

'expected_return': expected_return,

'volatility': volatility,

'sharpe_ratio': sharpe_ratio

}

return result

Kết luận

Trong bài viết này, chúng ta đã tìm hiểu cách sử dụng Python để thực hiện phân tích rủi ro và lợi nhuận danh mục đầu tư. Từ việc thu thập dữ liệu, tính toán các thước đo rủi ro, xây dựng mô hình tối ưu hóa danh mục theo lý thuyết Markowitz, cho đến kiểm định sức chịu đựng và tái cân bằng danh mục.

Các phương pháp và công cụ này giúp nhà đầu tư ra quyết định đầu tư dựa trên dữ liệu, cân bằng giữa rủi ro và lợi nhuận kỳ vọng, từ đó xây dựng chiến lược đầu tư hiệu quả và phù hợp với mục tiêu tài chính.

Lưu ý rằng kết quả phân tích dựa trên dữ liệu lịch sử không đảm bảo hiệu suất trong tương lai. Nhà đầu tư nên kết hợp các phương pháp phân tích khác và cập nhật chiến lược định kỳ để thích ứng với điều kiện thị trường thay đổi.

Tài liệu tham khảo

- Markowitz, H. (1952). Portfolio Selection. The Journal of Finance, 7(1), 77-91.

- Sharpe, W. F. (1964). Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk. The Journal of Finance, 19(3), 425-442.

- Hull, J. C. (2018). Risk Management and Financial Institutions (5th ed.). Wiley.

- Python for Finance: Mastering Data-Driven Finance (2nd ed.) by Yves Hilpisch

- Yahoo Finance API Documentation: https://pypi.org/project/yfinance/